IFSC Third-Party Fund Management Framework: Why This Matters for GIFT City Managers

IFSCA’s third-party fund management framework opens a platform-play route for GIFT City managers, but the opportunity comes with authorisation, fees, governance, liability, and scheme-structure implications.

- ifsca

- gift city

- third-party fund management

- fund management entity

- ifsc funds

- platform play

The most important word in IFSCA’s third-party fund management framework is not “third-party.”

It is “platform.”

For years, one practical question has sat behind many GIFT IFSC fund conversations: does every fund manager need to build a full IFSC presence before testing a strategy, launching a restricted scheme, or accessing the IFSC ecosystem?

IFSCA’s third-party fund management framework gives a more flexible answer.

On June 24, 2025, IFSCA approved amendments to facilitate third-party fund management services, commonly described as a “platform play” model. Mondaq’s coverage explained that registered Fund Management Entities in IFSC can launch and manage restricted schemes on behalf of domestic or overseas third-party fund managers without requiring those third-party managers to establish physical presence in the IFSC.

The notified framework followed through in July 2025. Mondaq later noted that IFSCA notified the Fund Management Amendment Regulations on July 24, 2025, operationalising the third-party fund management framework and allowing global fund managers to use the platform of existing FMEs.

Commercially, this matters because it creates a lower-friction entry route.

A global manager, boutique asset manager, emerging sponsor, family-office-backed strategy, or first-time fund manager may not want to immediately build a full IFSC operating entity, hire a full local team, maintain independent infrastructure, and carry the full cost of direct setup. A platform model allows them to work through an authorised FME that already has the regulatory base in GIFT IFSC.

That can make GIFT City more attractive.

But this is not a casual hosting arrangement. The framework is commercially useful precisely because it is regulated. Managers should read it as an opportunity with guardrails, not as a shortcut around governance.

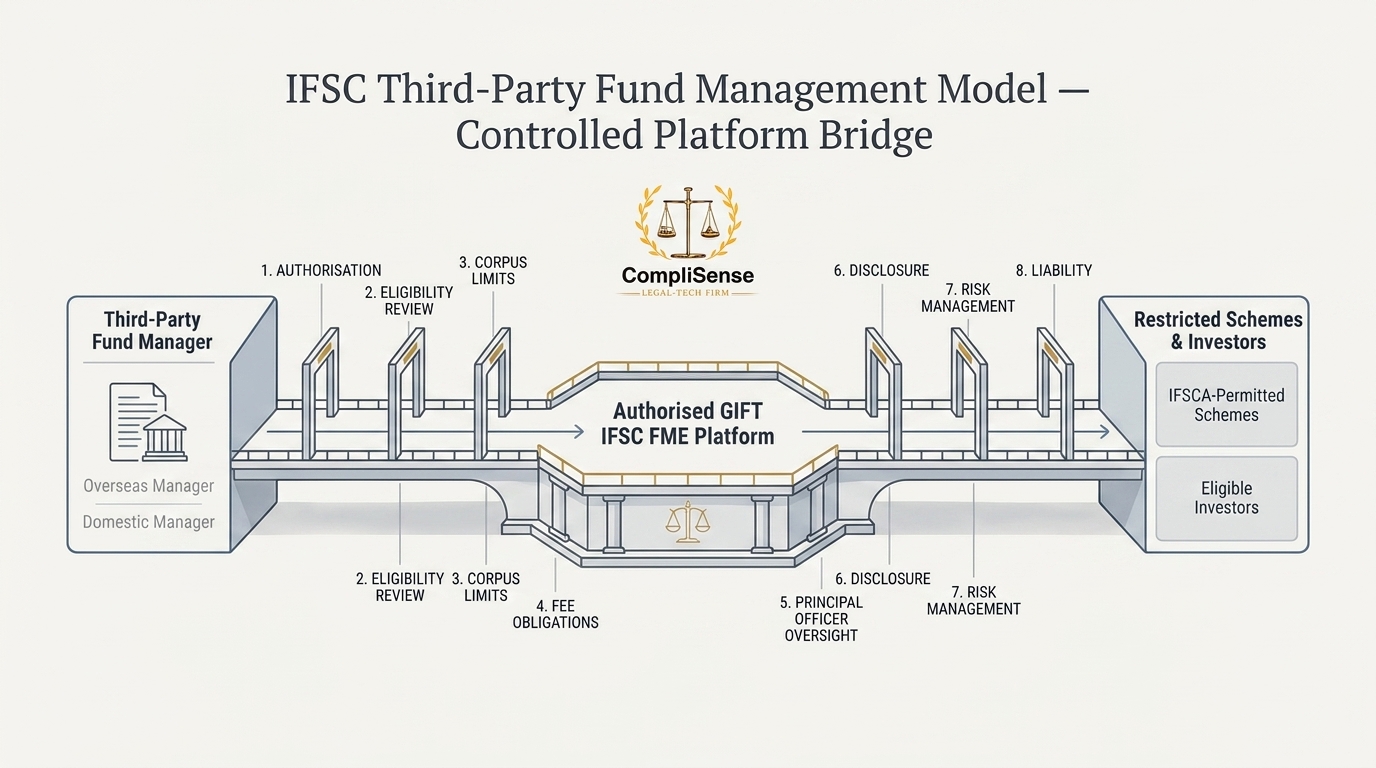

The first implication is authorisation.

An FME cannot simply start offering third-party fund management services because it has an existing registration. FMEs need specific authorisation from IFSCA, and if the FME is set up as a company or LLP, its charter documents must enable such third-party fund management services.

That means existing FMEs should begin with a platform-readiness review.

Do the constitutional documents permit this activity?

Does the business plan support platform services?

Is the FME prepared to supervise outside managers?

Does it have the people, policies, and controls to manage multiple third-party relationships?

If not, the platform opportunity can become a regulatory burden.

The second implication is eligibility of the third-party fund manager.

The framework is not open to just anyone with a fund idea. Mondaq’s summary notes that third-party fund managers should be incorporated in India, IFSC, or a foreign jurisdiction; should allocate adequate resources; should have responsible persons with adequate experience; and their officers, directors, partners, KMPs, and controlling shareholders should be fit and proper.

So the FME needs a serious onboarding process.

A good platform FME should not treat third-party managers as ordinary clients. It should review regulatory status, ownership, track record, investment capability, key personnel, conflicts, adverse history, and operating capacity. If the third-party manager fails later, the FME will not be able to say, “They were only using our platform.”

That brings us to the most important compliance implication: liability.

Under the framework, the FME assumes responsibility for obligations connected with the third-party fund management service, irrespective of any indemnity arrangement with the third-party fund manager. Mondaq’s coverage also notes that the FME is responsible for acts of omission and commission of the third-party in relation to the service, and that the schemes are treated as schemes of the FME.

This is the trade-off.

The third-party manager gets market access and speed. The FME gets platform revenue and business scale. But the FME also carries supervisory responsibility.

That means the commercial contract cannot be the only control document. The FME needs an internal policy for third-party fund management, conflict identification, operational independence, investor grievance handling, internal audit/review, and ongoing supervision. The framework specifically expects risk-management measures around eligibility, monitoring, termination rights, periodic review, indemnity, and compliance with IFSCA requirements.

The third implication is economics.

IFSCA’s fund-management page lists the September 8, 2025 circular on the fee structure applicable for third-party fund management services. Mondaq’s September 2025 update states that registered FMEs offering third-party fund management services must pay an application fee of USD 2,500, an authorisation fee of USD 7,500, and an annual conditional recurring fee of USD 2,000 per third-party fund manager from the financial year following contract execution; these fees are in addition to the earlier flat recurring fee of USD 2,000.

This matters for pricing.

FMEs should not price platform services only as a commercial hosting fee. They need to factor in authorisation cost, recurring fees, additional net worth, incremental personnel, internal review, legal documentation, compliance monitoring, audit effort, investor servicing, and liability risk.

A low platform fee may look attractive at launch but become uneconomic once supervision starts.

The fourth implication is scheme structure.

The framework is focused on restricted schemes. Mondaq’s coverage states that restricted schemes launched under third-party fund management can have a maximum corpus of USD 50 million, and given the USD 3 million minimum corpus for restricted schemes, the corpus range effectively sits between USD 3 million and USD 50 million.

This makes the model especially relevant for emerging managers and focused strategies. It can help test an IFSC thesis without immediately building a large platform. But managers should be realistic: the corpus cap means this is not the right structure for every strategy.

The fifth implication is people.

The framework requires personnel discipline. A separate principal officer must be appointed for every scheme managed under a third-party fund management arrangement, with responsibility for overall scheme activities including fund management, risk management, and compliance. Compliance officer requirements also apply, with separate treatment for Registered FME Non-Retail and Retail categories.

This is where implementation may pinch.

A platform FME may be tempted to onboard multiple third-party managers quickly. But each additional arrangement adds oversight complexity. Who reviews the strategy? Who monitors restrictions? Who checks disclosures? Who handles investor grievances? Who signs off conflicts? Who tracks reporting?

The answer cannot be “the third-party manager will handle it.”

The FME must build the operating layer.

For GIFT City managers, the practical takeaway is clear: this framework creates a commercial opportunity, but the winners will be platform operators with discipline.

A serious FME should prepare five things before scaling this model:

An authorisation and charter-document readiness file.

A third-party manager onboarding and due-diligence checklist.

A fee and pricing model that reflects regulatory cost and liability.

A scheme-level governance matrix with principal officer and compliance ownership.

An ongoing supervision record covering conflicts, disclosures, investor complaints, reviews, and termination triggers.

The platform-play model can help GIFT IFSC compete with global fund centres by giving managers a faster, more flexible entry route. But the framework is not saying, “Outsource the manager and forget the risk.”

It is saying, “Use the platform, but keep the accountability.”

That distinction is where GIFT City managers should focus.

Related compliance hubs

Continue from this explainer into topic hubs that connect analysis with regulator updates and workflow context.

Related regulator archives

Continue into source-linked archives for regulators connected to this topic area.

Related legal updates

Source-linked updates that place this article in the current regulatory workflow.

Content accountability

Prepared by CompliSense Editorial Desk (Regulatory Content Team) and reviewed by CompliSense Regulatory Review Desk (Compliance Review Team).

This attribution reflects the preparation and review roles used for CompliSense regulatory publishing.