IFSCA Fund Management Regulations, 2025: What GIFT IFSC Participants Should Note

IFSCA’s 2025 Fund Management Regulations reshape the IFSC fund framework with clearer FME categories, easier scheme thresholds, and sharper governance expectations for funds and managers.

- ifsca

- gift ifsc

- fund management regulations 2025

- fund management entity

- ifsc funds

- alternative investment funds

The IFSCA Fund Management Regulations, 2025 should not be read as a routine regulatory update.

They are better understood as a maturity signal for GIFT IFSC’s fund ecosystem.

For fund managers, sponsors, family offices, portfolio managers, and institutions evaluating IFSC structures, the important question is not only “what changed?” The better question is: what kind of fund management platform is IFSCA trying to build?

The answer is visible in the design of the framework. IFSCA has moved towards clearer categories, lower entry friction in selected areas, broader product flexibility, and stronger governance expectations. That combination matters because fund regulation is always a balance between market development and investor protection.

IFSCA’s April 2025 transition circular states that the Fund Management Regulations, 2025 were published in the Official Gazette on February 19, 2025, repealing the 2022 framework. The circular also notes two practical changes for Venture Capital Schemes and Restricted Schemes: PPM validity moved from 6 months to 12 months, and minimum corpus reduced from USD 5 million to USD 3 million.

That is the headline. But the real story is the architecture underneath.

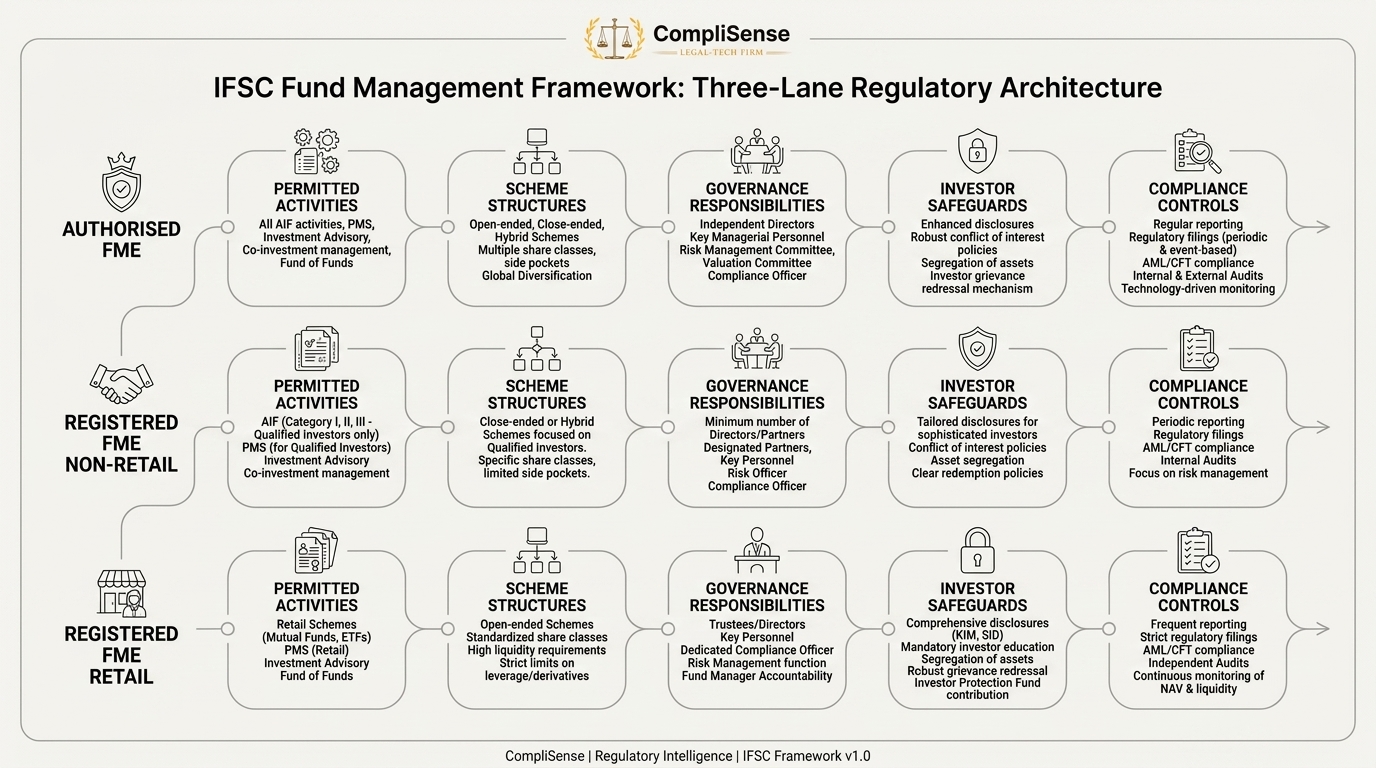

The new framework continues to organise fund management through the Fund Management Entity, or FME. This is important because the regulatory focus is not only on the fund product. It is also on the manager: who is managing money, what activities they can undertake, what governance they must maintain, and what obligations follow.

The regulations set out three broad FME categories.

An Authorised FME is positioned for venture capital schemes and single-family investment funds. A Registered FME Non-Retail can manage restricted schemes, undertake portfolio management services, act as investment manager for private placement REITs and InvITs, and also undertake Authorised FME activities. A Registered FME Retail can manage retail schemes, act as investment manager for public offer REITs and InvITs, launch ETFs, and also undertake activities available to the lower categories.

This tiered structure is useful because it gives participants a clearer route map. A manager does not need to view IFSC fund regulation as one large undifferentiated regime. The intended product, investor base, distribution model, and activity scope should determine the FME category.

That is the first practical point for participants: choose the category by business plan, not by regulatory label.

If the aim is a restricted private placement strategy, the compliance design will look different from a retail-facing scheme or ETF platform. If the aim is PMS, REIT/InvIT management, family investment structures, or venture capital, the operational assumptions also change. The wrong registration strategy can create friction later in staffing, disclosures, governance, and permitted activity.

The second point is that the 2025 framework is not only liberalising. It is also formalising governance.

For example, the regulations require an FME applicant to be set up in IFSC as a company, LLP, branch, or another permitted form, but a Registered FME Retail cannot be an LLP or branch. A Registered FME Retail must also have at least four directors, with at least 50 percent independent directors. Branch structures are available only where the FME is already registered or regulated in India or a foreign jurisdiction for similar activities.

That tells participants something important: governance form is part of the regulatory assessment. It is not enough to have an investment strategy and investor interest. The operating entity itself must be credible.

The third point is personnel discipline.

The regulations require a principal officer responsible for overall FME activities, including fund management, risk management, and compliance. Registered FMEs also need a compliance officer responsible for compliance and implementation of risk management policies. Retail FMEs need an additional KMP before filing the offer document for the first retail scheme or ETF. FMEs managing at least USD 1 billion AUM, excluding fund-of-funds schemes, must appoint another KMP for fund management within the specified timeline.

This is where many participants should be careful. GIFT IFSC is attractive because it can offer structuring flexibility, global investor access, and a specialised financial centre environment. But it is not a light-touch “paper presence” model. Serious fund management needs serious people, defined roles, and documented accountability.

The fourth point is that reduced thresholds should not be confused with reduced discipline.

Lower minimum corpus requirements and longer PPM validity can help managers launch and operationalise schemes more realistically.

That is a fair way to read the development. The framework is opening doors, but not removing control expectations.

This is especially clear in the conduct and risk provisions. The regulations require registered FMEs to maintain business continuity planning, cyber security and cyber resilience frameworks, sound risk management systems, and adequate internal controls based on the business undertaken, including outsourced activities.

For fund managers, that means the launch checklist should not stop at registration, PPM, investor onboarding, and bank accounts. It should include a living operating model: risk policy, outsourcing oversight, valuation process, investor communication, cybersecurity readiness, records, conflict management, escalation, and reporting.

The fifth point is investor protection.

The code of conduct provisions make the FME responsible for due diligence, employee and service-provider conduct, compliance, valuation, fair investor information, ring-fencing of scheme assets and liabilities, AML/CFT compliance, and high standards of integrity and professional judgment.

This matters because GIFT IFSC is competing as an international financial center. Investors will look not only at tax, access, and fund strategy, but also at governance quality. A weak back office, unclear valuation process, unmanaged conflicts, or poor disclosure discipline can damage credibility even where the investment thesis is strong.

The sixth point is that managers should prepare for supervision, not just approval.

The regulations allow IFSCA to inspect books, accounts, records, documents, infrastructure, procedures, and systems of an FME or related entities to check compliance. This means participants should build records as they operate, not reconstruct them when a query arrives.

For GIFT IFSC participants, the practical takeaway is this:

Do not treat the 2025 regulations as only an opportunity to launch faster. Treat them as a blueprint for building a credible IFSC fund management business.

That means choosing the correct FME category, mapping permitted activities, appointing the right KMPs, documenting risk and compliance responsibilities, setting up investor disclosure discipline, ring-fencing scheme assets, maintaining records, and building internal controls before scale arrives.

The 2025 framework should help funds and managers that want a serious IFSC platform. But it will not reward casual implementation. The entities that benefit most will be the ones that pair regulatory flexibility with institutional governance.

GIFT IFSC’s fund opportunity is real. The compliance test is whether participants can build structures that are not only approved, but also durable, supervised, and investor-ready.

Related compliance hubs

Continue from this explainer into topic hubs that connect analysis with regulator updates and workflow context.

Related regulator archives

Continue into source-linked archives for regulators connected to this topic area.

Related legal updates

Source-linked updates that place this article in the current regulatory workflow.

Content accountability

Prepared by CompliSense Editorial Desk (Regulatory Content Team) and reviewed by CompliSense Regulatory Review Desk (Compliance Review Team).

This attribution reflects the preparation and review roles used for CompliSense regulatory publishing.