XBRL and Integrated Filing Changes: What Listed Entities Need to Get Right

XBRL-based integrated financial filing is not just a format change. Listed entities need stronger filing discipline, cleaner data, tighter coordination, and fewer last-minute errors.

- xbrl filing

- integrated filing financial

- listed entity compliance

- sebi lodr

- nse filing

- bse filing

The mistake listed entities should avoid is treating XBRL-based integrated filing as a “format change.”

It is not just that.

It is a discipline change.

From April 1, 2025, NSE and BSE moved listed entities towards XBRL-based Integrated Filing-Financial. Mondaq also noted this shift in its regulatory reform coverage, and NSE’s circular stated that listed entities are required to submit financial results in XBRL mode using the “Integrated Filing-Financial” utility only.

That sounds like a technical filing update. In practice, it changes the pressure points inside the company.

Earlier, many filing processes were built around document preparation: finalise the board outcome, prepare the PDF, attach schedules, check signatures, upload within the prescribed timeline, and keep proof. XBRL filing is less forgiving because the data itself has to be structured correctly. If the underlying numbers, classifications, labels, periods, schedules, and cross-references are not clean, the problem does not appear as a drafting issue. It appears as a validation issue, a mismatch, or a filing defect.

And those defects usually appear at the worst possible time.

On financial results day, the company secretary, finance team, CFO office, auditors, board support team, and exchange filing team are already working under pressure. The board meeting has concluded. The outcome needs to be filed. Financial results need to go out. Investor-facing information must be consistent. Every minute matters.

That is not the time to discover that one figure does not reconcile, one schedule was prepared on an older version, one field owner is unavailable, or one XBRL validation error has no clear internal owner.

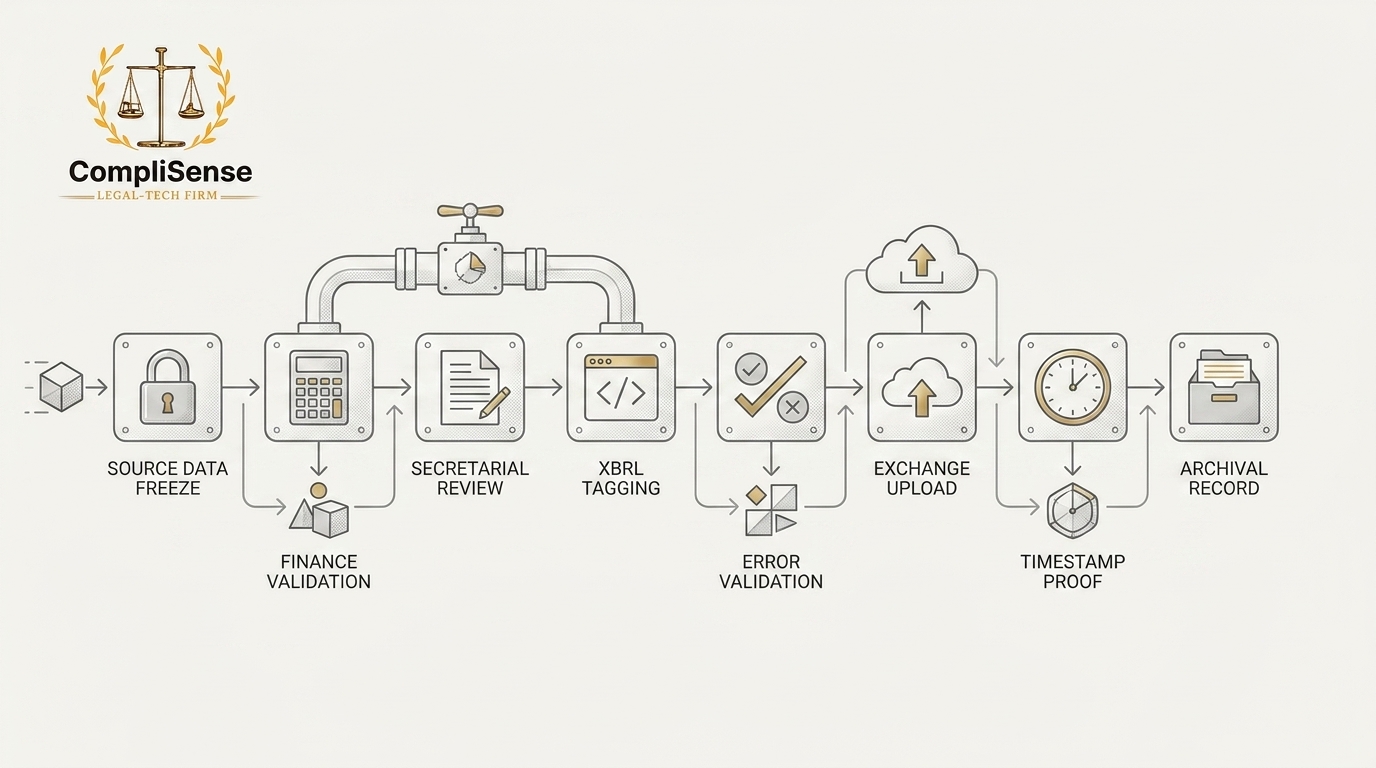

The practical lesson is simple: listed entities should move the quality control earlier.

The first thing to get right is data ownership. Every data point in an integrated financial filing should have a source owner. Finance may own the financial statements. Secretarial may own governance-linked disclosures. Legal may review certain event-based statements. The CFO office may approve final numbers. But the filing team should not be forced to guess who owns which field.

If a value appears in the XBRL filing, someone should know where it came from, who checked it, and whether it matches the board-approved version.

The second issue is version control. This is where avoidable errors are born. Financial results may go through multiple drafts. Notes may change. Auditor comments may lead to revisions. Board packs may have a near-final version. The final signed version may differ slightly from the working version. If the XBRL preparation is done on the wrong version, the filing team may upload technically structured but substantively incorrect data.

A modern filing process needs a clear “data freeze” point. Once the board-approved numbers are final, the team should know which version is the source of truth. No parallel Excel sheets. No WhatsApp-circulated corrections. No informal “use this one instead” unless the change is recorded and rechecked.

The third issue is reconciliation. XBRL does not remove the need for human review. It increases the need for disciplined review. The figures in the XBRL utility should reconcile with the board-approved financial results, PDF outcome, notes, related disclosures, and any other connected filing.

This is especially important because integrated filing is meant to bring multiple disclosure elements into a more structured submission environment. NSE’s January 2025 circular referred to Integrated Filing-Financial timelines of 45 days from quarter-end, except the last quarter and financial year where the timeline is 60 days, and also mapped items such as financial results, related party transaction disclosures, statement of deviation and variation, and quarterly disclosure of outstanding default on loans or debt securities into the Integrated Filing-Financial framework.

That means listed entities should not look at the financial result in isolation. The filing pack has to be internally consistent.

The fourth issue is validation planning. Many teams treat validation errors as a last-step inconvenience. That is risky. Validation should be treated as a control stage. The person resolving the error should understand whether it is merely a formatting issue, a tagging issue, a missing field, a period mismatch, or a substantive data inconsistency.

Not all errors are equal. Some can be fixed by correcting the input. Some require finance confirmation. Some require secretarial review. Some may need escalation because the underlying disclosure itself is unclear.

If the filing team does not classify errors properly, speed can become dangerous.

The fifth issue is internal coordination. Integrated filing sits between finance and compliance, but it cannot be owned casually by either side alone. Finance knows the numbers. Secretarial and compliance understand the filing obligation. Legal may understand sensitive disclosures. Senior management owns the seriousness of the market-facing communication.

This requires a short, disciplined filing protocol.

Before every results cycle, the company should know who will prepare the data, who will review it, who will run XBRL validation, who will approve final upload, who will keep timestamp proof, and who will archive the filed version.

This does not need a 40-page SOP. It needs a clear operating sheet that people actually follow.

Listed entities should also train teams not to see XBRL as “someone else’s portal work.” The quality of the XBRL filing depends on the quality of internal data discipline. If the upstream data is messy, the filing team inherits the mess. If ownership is unclear, the filing team becomes the bottleneck. If review happens too late, the company runs close to the deadline with avoidable pressure.

The change should therefore push listed entities to professionalise their financial filing process.

The real question for management is not: “Can our team upload XBRL?”

The better question is: “Can our team produce a clean, reconciled, approved, timestamped, and defensible integrated filing without last-minute confusion?”

That is the standard.

XBRL makes filing more structured. Integrated filing makes the submission more consolidated. But neither of them automatically makes the company more disciplined. That part still depends on internal process.

For listed entities, the immediate priority is clear: clean the data chain, assign field ownership, freeze the correct version, validate early, reconcile before upload, and preserve evidence.

Filing errors are rarely caused by the final upload button. They are usually created much earlier, when data ownership, version control, and internal coordination are weak.

That is where listed entities need to focus now.

Related compliance hubs

Continue from this explainer into topic hubs that connect analysis with regulator updates and workflow context.

Related regulator archives

Continue into source-linked archives for regulators connected to this topic area.

Related legal updates

Source-linked updates that place this article in the current regulatory workflow.

Content accountability

Prepared by CompliSense Editorial Desk (Regulatory Content Team) and reviewed by CompliSense Regulatory Review Desk (Compliance Review Team).

This attribution reflects the preparation and review roles used for CompliSense regulatory publishing.