SEBI’s Insider-Trading Compliance Changes for Immediate Relatives: Why Internal Controls Need an Update

SEBI’s move to extend automated trading-window closure to immediate relatives makes insider-trading compliance more data-driven. Listed entities now need stronger declarations, awareness, and control discipline.

- insider trading compliance

- immediate relatives

- designated persons

- sebi pit regulations

- trading window closure

- listed entity compliance

For many listed entities, insider-trading compliance around immediate relatives has historically depended on one fragile assumption: the designated person will remember, understand, and control what their immediate relatives do.

That assumption is no longer good enough.

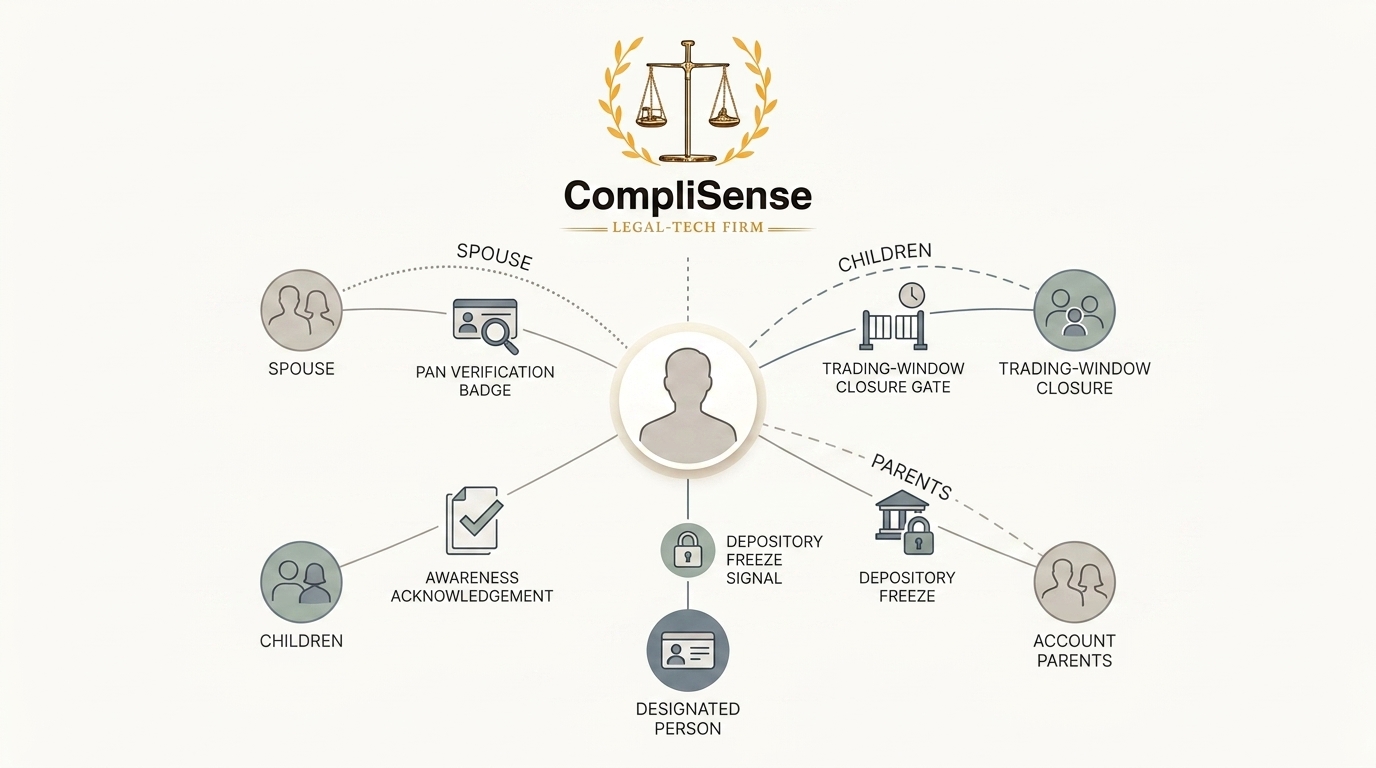

SEBI’s April 21, 2025 circular extended automated implementation of trading-window closure to immediate relatives of designated persons, specifically in relation to declaration of financial results. The circular applies the framework through PAN-level restrictions at the security level, with phased implementation for the top 500 companies from July 1, 2025 and remaining listed companies from October 1, 2025.

This is not just a legal update. It is a control-design update.

The earlier model placed a heavy burden on internal reminders and personal discipline. The compliance officer would close the trading window, send communication to designated persons, and expect them to ensure that their immediate relatives also did not trade. That process was always vulnerable to weak declarations, delayed communication, family-level misunderstanding, outdated PAN details, and informal assumptions.

The new framework reduces some of that weakness by moving immediate relatives into the automated restriction system. But automation only works if the underlying data is accurate.

That is where listed entities need to focus now.

The first internal control to update is the declaration process.

Immediate-relative details should not be treated as an annual formality. If the company does not have correct PAN information, demat account linkage details where relevant, relationship records, and change history, the automated freeze may not operate properly. SEBI’s process requires listed companies to confirm details such as ISIN, name, PAN, and demat account information for designated persons and their immediate relatives through the Designated Depository process.

That means the declaration form has become more important than before. A weak declaration is no longer just a paperwork issue. It can directly affect whether the control actually works.

Listed entities should review whether their current declaration format asks the right questions. It should capture spouse, parent, sibling, and child relationships where covered under the PIT Regulations, but it should also force the designated person to think practically: who is financially dependent, who consults them on trading decisions, who has a demat account, and whether any details have changed since the last declaration.

The second control is update frequency.

Many companies collect declarations once a year and then leave the record untouched unless someone remembers to update it. That is risky. Family circumstances change. Demat accounts are opened. Dependence changes. Relatives may start trading. Employees move into or out of designated roles. If the database is stale, the control is stale.

A better approach is event-based updating. At minimum, designated persons should confirm immediate-relative details before every quarterly trading-window closure cycle. HR and secretarial teams should also trigger updates when a person becomes designated, moves into a sensitive role, exits the company, or is added to a UPSI-linked project.

The third control is the trading-window calendar.

Under the SEBI framework, for financial results, the listed company has to specify the commencement date and end date of the trading-window closure period on the portal/platform. The closure begins from the first day immediately after the end of the quarter and ends 48 hours after disclosure of financial results. The required details must be provided at least two trading days before commencement.

This makes calendar discipline critical.

The company secretary or compliance officer should not be calculating closure dates at the last minute. The board meeting calendar, result approval timeline, closure commencement date, depository portal deadline, internal communication date, and reopening date should be mapped before the quarter closes.

The fourth control is awareness.

Automation does not remove the need for education. In fact, it makes education more important because designated persons need to understand that immediate-relative information is now operationally significant. Wrong or incomplete information can create compliance gaps, trading restrictions, complaints, or unnecessary exceptions.

Awareness communication should be simple. Avoid sending only a legal extract from the code of conduct. Tell designated persons clearly:

Your immediate-relative declaration must be accurate.

You must update changes promptly.

Your relatives may be restricted during trading-window closure.

Do not assume that family trades are outside the compliance framework.

Ask compliance before there is a problem, not after a trade.

That message is more useful than a long legal circular nobody reads properly.

The fifth control is exception handling.

SEBI’s process recognises that exemptions may be specified in the system where permitted under the PIT framework, and restrictions can be removed within the prescribed operational timeline where valid exemptions are processed. But internally, exemptions should not become casual approvals.

Every exemption request should have maker-checker review, legal/compliance reasoning, date limits, supporting documents, and clear evidence of approval. If an exemption is granted, the company should know who requested it, why it was granted, who approved it, when it was sent for system action, and when the restriction was restored.

The sixth control is responsibility mapping.

This update is not only a compliance officer’s problem. HR may maintain employee and role data. Secretarial teams may manage board/result timelines. Finance may drive result finalisation. Designated persons provide immediate-relative details. Depository coordination may sit with the company secretary’s office or RTA-linked processes.

If the company does not map responsibility clearly, the control will break between teams.

Listed entities should create a simple internal ownership sheet for the quarterly cycle: who updates designated person records, who collects immediate-relative confirmations, who validates PAN details, who confirms closure dates, who updates the Designated Depository portal, who sends internal communication, who handles exceptions, and who preserves evidence.

The final control is evidence.

For every trading-window cycle, the company should retain the declaration status, communication sent, closure dates, portal confirmation, exception log, reopening communication, and any change requests. This is not just for audit comfort. It is how the company proves that the control operated.

The bigger point is this: SEBI has moved immediate-relative compliance from a soft reminder model towards a system-supported restriction model. Mondaq’s coverage also frames the circular as an enhancement of the insider-trading compliance framework around designated persons and immediate relatives.

That shift should push listed entities to redesign their internal controls.

Related compliance hubs

Continue from this explainer into topic hubs that connect analysis with regulator updates and workflow context.

Related regulator archives

Continue into source-linked archives for regulators connected to this topic area.

Related legal updates

Source-linked updates that place this article in the current regulatory workflow.

Content accountability

Prepared by CompliSense Editorial Desk (Regulatory Content Team) and reviewed by CompliSense Regulatory Review Desk (Compliance Review Team).

This attribution reflects the preparation and review roles used for CompliSense regulatory publishing.