NSDL’s New Requirement for Transfer of Dematerialised Shares of Private Companies

NSDL’s June 2025 circular adds a company-consent layer before off-market transfers of dematerialised private-company shares. Private companies, shareholders, investors, and DPs need tighter documentation discipline.

- nsdl

- demat shares

- private company shares

- share transfer

- depository participant

- company consent

For private companies, dematerialisation solved one problem and exposed another.

The transfer could move electronically through the depository system. But the company’s internal transfer restrictions — Articles of Association, shareholder arrangements, board approval requirements, right of first refusal clauses, and other consent mechanics — could still sit outside the DP’s actual execution flow.

That gap is exactly where NSDL’s June 2025 circular matters.

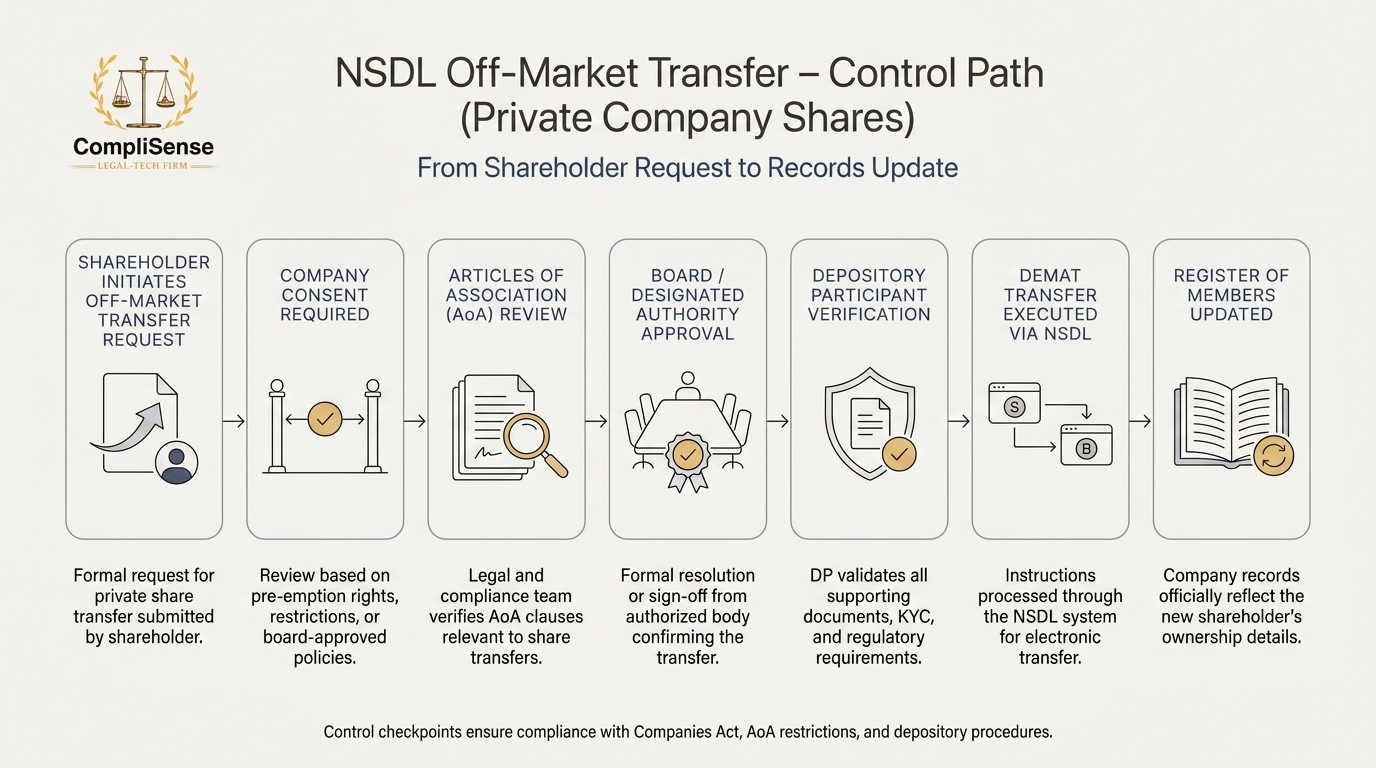

NSDL Circular No. NSDL/POLICY/2025/0071 dated June 3, 2025 introduced an additional requirement for off-market transfers of shares of private limited companies held in dematerialised form. Going forward, a demat account holder seeking to transfer such shares through NSDL must submit a consent or confirmation letter from the company to the Depository Participant, along with the Delivery Instruction Slip.

This is a narrow change, but it is not a small one.

Before this, the seller could submit a DIS to the DP with the transfer details, and the depository transfer process could proceed even though the DP had no practical way to verify whether the transfer complied with the company’s Articles or shareholder-level restrictions. Argus Partners noted that this could leave private companies receiving only post-facto intimation of transfers, despite restrictions under the Articles or shareholder arrangements.

The circular effectively inserts the private company back into the transfer chain.

That means the affected parties are clear.

Private limited companies whose shares are held in demat form are affected because they now need a mechanism to review and issue consent or confirmation. Shareholders are affected because they cannot treat the DP transfer step as only a DIS submission. Buyers, investors, and transaction teams are affected because closing timelines may now depend on company-side confirmation. DPs are affected because they must check for the prescribed consent before processing the transfer.

This is especially relevant for promoter transfers, investor exits, secondary transfers, employee or ESOP-related transfers where shares are dematerialised, intra-group transfers, family transfers, and private equity or venture capital secondary transactions.

The first document to focus on is the company consent or confirmation letter.

The consent letter must confirm that the proposed transfer complies with the Companies Act, 2013 and that necessary internal approvals, such as board approvals or compliance with the Articles of Association, have been obtained. It must also include transferor and transferee demat account details, PAN details, number of shares proposed to be transferred, and the reason for the transfer.

That sounds administrative. In practice, it creates a control checkpoint.

A private company should not issue the confirmation casually. Before signing it, the company should check whether the Articles restrict transfer, whether board approval is needed, whether any shareholder agreement consent applies, whether existing investors have pre-emptive rights, whether the transferee is permitted, whether consideration and transaction purpose are documented, and whether the company’s register and beneficial ownership records will need updating.

The friction will begin where companies have no internal process.

If the Articles require board approval, who calls the board meeting or passes the circular resolution? If investor consent is required, who checks the shareholder agreement? If the transfer is urgent, who confirms whether any right of first refusal period has expired or been waived? If the transfer is between relatives or group entities, who verifies whether it still requires approval? If the transferee’s demat details are incorrect, who coordinates correction?

None of these are DP questions. These are company-side control questions.

Another likely friction point is timing.

Argus Partners observed that the circular introduces a prior consent requirement but does not appear to prescribe a formal process or time limit for companies to provide consent, which may increase timelines for shareholders wanting to complete transfers.

That matters for deals. Transaction documents often assume that demat transfers can be completed quickly once conditions precedent are satisfied. Now, for NSDL-held private-company shares, the transaction checklist should include company consent as a separate closing item. If the consent is not built into the timeline, the deal team may discover the requirement only at the DP execution stage.

The practical solution is simple: do not leave the consent letter for the last day.

For every proposed transfer, teams should create a short pre-transfer checklist:

Is the company private limited?

Are the shares held in demat form through NSDL?

Is the transfer off-market?

Does the Articles of Association restrict transfer?

Is board approval required?

Are investor or shareholder consents required?

Are transferor and transferee demat and PAN details verified?

Has the reason for transfer been recorded?

Has the company issued the prescribed confirmation?

Has the final transfer been reflected in company records?

This is the minimum operating discipline.

Private companies should also keep a consent register. Every consent issued should be traceable: date of request, transferor, transferee, number of shares, basis of approval, board or shareholder approval reference, consent letter copy, DP submission status, and final completion status.

This protects the company later if a dispute arises.

For DPs, the requirement is more straightforward but still important. The DP should not process an off-market transfer of dematerialised shares of a private company unless the prescribed company confirmation accompanies the DIS. Mondaq’s coverage states that DPs will no longer be permitted to process such transfers unless the company has issued the prescribed confirmation letter.

For shareholders and investors, the lesson is equally direct: share transfer rights on paper are not enough. The execution path now needs cooperation from the company. Transaction documents should therefore require timely issuance of the company confirmation letter and should define who is responsible for obtaining it.

This is not merely a procedural hurdle. It is NSDL aligning the demat transfer process with the legal character of a private company, which under Section 2(68) of the Companies Act, 2013 restricts the right to transfer its shares. Argus describes the circular as operationalising that legal restriction in the depository process.

One caution is important: available commentary notes that this requirement has been notified by NSDL, and that no corresponding CDSL requirement had been prescribed at the time of those updates. Teams should still check the latest depository position before execution, especially where holdings are split or where the transferee’s account is with another depository.

The practical takeaway is narrow but important.

Private-company demat share transfers can no longer be treated as only a shareholder-DP instruction flow. The company’s consent, internal approvals, Articles check, and documentation trail now need to be built into the transfer process.

For private companies, this is a chance to regain control over unauthorised or non-compliant transfers.

For shareholders and investors, it is a new execution dependency.

For compliance and legal teams, it is a reminder that demat does not eliminate corporate law controls. It only changes where those controls must be enforced.

Related compliance hubs

Continue from this explainer into topic hubs that connect analysis with regulator updates and workflow context.

Related regulator archives

Continue into source-linked archives for regulators connected to this topic area.

Related legal updates

Source-linked updates that place this article in the current regulatory workflow.

Content accountability

Prepared by CompliSense Editorial Desk (Regulatory Content Team) and reviewed by CompliSense Regulatory Review Desk (Compliance Review Team).

This attribution reflects the preparation and review roles used for CompliSense regulatory publishing.